The Aging Roof That Nearly Cost a Homeowner Their Policy

Most homeowners assume a roof only earns attention when it starts to leak. The reality is harsher, because an insurer can force a roof replacement Liberty TX owners never budgeted for, long before a shingle ever fails. One aging roof and one renewal letter can put an entire policy at risk.

One Renewal Letter Changed the Plan

The homeowner in this case had a 2000s-era house near Liberty, Texas, and a roof pushing twenty years. Nothing leaked, and nothing looked wrong. Then the renewal notice arrived, and the carrier wanted the aging roof replaced or the policy would lapse. That surprised them, but it fits what the market has been doing for a while now. My Neighborhood News reported in January 2026 that Greater Houston homeowners saw milder 4 to 8 percent premium increases this year. That was a relief after the 19 to 21 percent spikes of 2023 and 2024, though rebuilding costs still sit 30 to 40 percent above pre-pandemic levels. Carriers are managing that exposure by scrutinizing the parts of a home most likely to fail. A two-decade roof sits near the top of that list.

Why Insurers Now Watch Roof Age

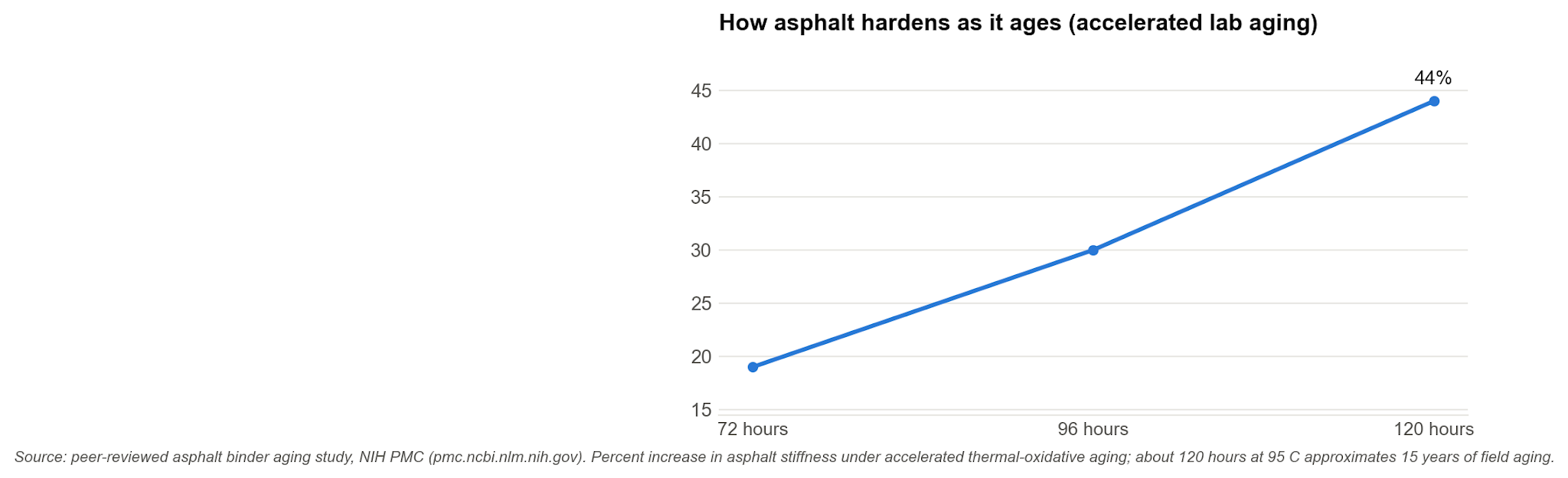

Roof age is not a proxy that carriers picked at random. It tracks a real material process that plays out slowly. Asphalt shingles harden and grow brittle as they oxidize in the Texas sun. The change is subtle at first, then it accelerates. A peer-reviewed asphalt binder aging study tracked the binder’s stiffness climbing 19 percent, then 30 percent, then 44 percent across longer aging intervals. In that accelerated test, roughly 120 hours at 95 degrees Celsius approximated about 15 years of real field exposure. An older shingle flexes less and cracks more, which is exactly the weakness a wind or hail event exploits.

The case we see most often is a roof that still looks fine from the driveway but has quietly lost the flexibility that once kept it watertight. That roof was living on borrowed time.

Insurers know the pattern, so they price and underwrite around it. A twenty-year roof in a hail-prone county is not a hypothetical to them, it is a claim waiting for the next storm. They have watched too many aged roofs fail in the same predictable way, season after season. The math is simple on their side of the table. One large hail claim can erase years of collected premium, so they would rather see the roof replaced on the homeowner’s schedule than on the storm’s. That is why the renewal letter, not the leak, is often the first real warning an owner gets. Acting before the stated deadline is what keeps a manageable project from turning into a dropped policy.

What the Replacement Timeline Looked Like

Once the homeowner decided to act, the project moved faster than they expected. The first week went to the inspection and a plain conversation about materials, since the goal was a roof the carrier would accept and one that would ease the summer cooling load. By day three of the actual work, the old shingles were off and the deck lay exposed, which is when hidden damage usually turns up. In this house it was minor, just a few soft spots near a valley. Crews replaced the decking, laid new underlayment, and set the energy-efficient shingles within 10 days of the tear-off starting. The final inspection and cleanup closed the job out. Photos and material specs went straight to the insurer, because documentation is what turns a finished job into a satisfied underwriter. Month one ended with the policy intact and a paper trail the carrier could not argue with.

Where the Cooling Savings Showed Up

The kept policy was only half the return. Reflective, energy-efficient shingles lower the attic temperature, which eases the load on an air conditioner that runs hard through a Southeast Texas summer. Homeowners comparing products can start with the free ENERGY STAR Roof Products finder, which lists reflective options by solar reflectance with no sales pitch attached. In this house, the difference showed up on the first full cooling bill after installation, modest but real. Over a full Texas cooling season, those trimmed afternoon peaks are the part a homeowner actually feels in the wallet. Reflective roofing does not turn a home into an icebox. It trims the peak, and over a twenty-year roof life that trim keeps adding up.

The Payoff Beyond a Kept Policy

The lesson here is not that every old roof triggers a crisis, but that roof age is now a live variable in whether a policy renews. The material you choose shapes that math too, and it deserves a moment of real thought. A 2026 homeowner survey published by Roofing Contractor put asphalt shingle on 69 percent of roofs, with tile at 13 percent, synthetics at 10 percent, and metal at 9 percent. Most owners end up replacing like for like on a familiar, insurable material. That familiarity works in your favor, because carriers understand asphalt and price it predictably. For any homeowner weighing a roof replacement Liberty TX insurers will actually accept, the move is to document everything and pick materials that satisfy both the underwriter and the August electric bill. A roof handled that way stops being a liability on the renewal form and starts being the asset it always should have been.

- A Seasonal Roof Checklist Every Rural Property Owner Needs - July 12, 2026

- Why Hand Tamping a Kennel Run Pad Costs More Than Renting a Roller - July 12, 2026

- How Homes With Big Dogs Wreck Their Siding Faster - July 12, 2026